Personal Loans 101

Choosing the right tools to meet your financial goals

If you happen to find yourself in a tight spot, borrowing money can help set you back on the right path. However, doing so without a full understanding of the facts can hinder your finances in the future.

“When faced with a financial emergency, most people don’t think through how borrowing money might affect them down the line,” said Susie Irvine, president and CEO, American Financial Services Association Education Foundation. “With so many options available, it’s relatively easy to get a loan, but the impact on your credit and what it actually costs you over time can vary a great deal.”

The two most common types of small-dollar borrowing are traditional installment loans and payday loans. Knowing the ins and outs of each type of loan and how they work can help you make the best decision for your financial situation.

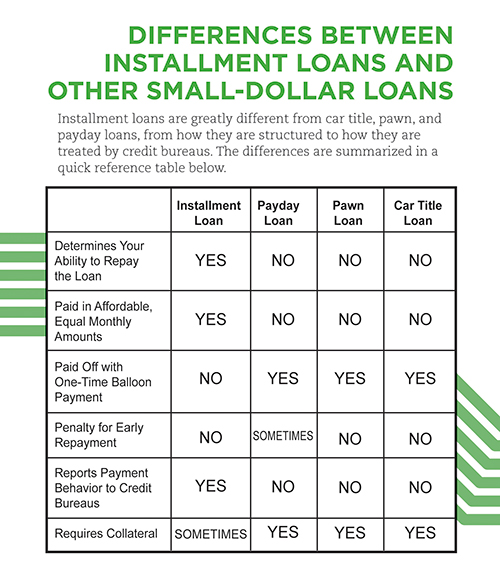

Traditional installment loans are one of the oldest forms of finance transactions and provide credit to individuals and families who need access to credit to meet an immediate need, such as vehicle repairs, household appliances or medical expenses. Averaging around $1,500, traditional installment loans are “plain vanilla” loans with transparent, easy-to-understand repayment terms, due dates and payment amounts – which usually average $120 per month over a term of about 15 months. With regular, manageable payments of principal and interest, the borrower has a clear roadmap out of debt. Best of all, traditional installment lenders report payment activity to credit bureaus, improving a borrower’s credit score when payments are made on time.

Payday loans are repaid in a single balloon payment at the end of the loan period. This payment is usually due in less than 30 days and frequently the term is as short as 14 days. Payday lenders do not assess ability to repay, relying instead on a postdated check or similar access to a borrower’s bank account as assurance the loan will be repaid. If a borrower cannot afford to repay a payday loan in full when it comes due, they are left with no option but to refinance the entire balance of the initial loan. Although payday loans may appear to provide a quick and easy solution, this single, lump-sum payment can lead to significant problems for the borrower. Payday lenders have also been sanctioned in many states, and at the federal level, for abusive practices.

Is an Installment Loan Right for You?

When deciding whether to obtain a loan, consider the benefits and responsibilities. According to the American Financial Services Association Education Foundation, an installment loan:

- Obligates future income. You’ll be required to set aside a certain amount of future income for loan payments.

- Requires discipline. Borrowing wisely means not borrowing more than you can handle. Don’t let the thrill of buying obligate you to more than you can afford.

- Makes it possible to meet unexpected expenses. The ability to borrow and make affordable payments can be helpful if an emergency arises that requires extra money.

- Allows you to obtain products and services now and pay for them later. A loan can provide an opportunity to purchase bigger-ticket items and use them right away.

Loan Language

When you take out a loan, it’s important to understand the complete cost of repaying the amount you’ve borrowed. It’s a good idea to compare offers from multiple creditors and understanding these terms will help you calculate the real cost of borrowing to get the best deal. Here is a list of common loan terms from the American Financial Services Association Education Foundation:

- Amount Financed: The total dollar amount of the credit that is provided to you.

- Annual Percentage Rate or “APR”: A measure of the cost of credit expressed as a yearly rate.

- Credit Insurance: Optional insurance that is designed to repay the debt if the borrower dies or becomes disabled.

- Finance Charge: The dollar amount you pay to use credit.

- Fixed Rate Financing: The interest rate and the payment remains the same over the life of the loan. Equal monthly payments of principal and interest are made until the debt is paid in full.

- Length of Payment: The total number of months you have to pay the credit obligation.

- Late Payment Fee: A fee that is charged when payment is made after its due date.

- Monthly Payment Amount: The dollar amount due each month to repay the credit agreement

Keys to Credit Success

The American Financial Services Association Education Foundation offers this advice to help ensure that your interests are protected when you borrow money:

Budget your money. Provide your monthly spending plan when you meet with creditors. It will help them make a responsible decision about the amount of credit you can afford.

Don’t overextend. Be sure you can pay back the loan. Don’t bite off more than you can chew.

Get personal. If possible, borrow from someone you actually can see and talk to in person. Get comfortable with the lender, and let the lender get comfortable with you.

Shop. Compare costs. Shop for credit like you would shop for anything else.

Beware of “now or never” offers. If it’s a good deal, it will probably still be there after you’ve had time to think about it. Don’t be pressured into making a quick decision.

Ask questions. Don’t sign on the line until all your questions have been answered.

Read the contract. Don’t sign a contract that you don’t understand or has any blanks. A signed contract with blanks can be completed as anyone wishes and it will be legally binding.

Keep your contract in a safe place. It’s important to keep all paperwork relating to your credit obligations. If questions come up later, you’ll have your agreement in writing.

Make your payments on time and in full. This is one of the best ways to build a good credit history.

Additional products are not required to get a consumer loan. Optional products that may be offered for purchase with your loan include motor club membership, term insurance or warranties.

To learn more about affordable credit options that are available to help you better manage your money, visit installmentloanswork.com.

Source:

AFSA

Save

{kind=link}